SWIFT

Our Services

What is SWIFT?

SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a global messaging network that enables financial institutions to securely exchange standardized financial messages, such as payment instructions, securities transactions, and account statements. It was founded in 1973 as a cooperative society under Belgian law, with the primary aim of replacing the telex-based communication systems that were previously used for international financial transactions. Today, SWIFT connects over 11,000 financial institutions across more than 200 countries, making it a key component of the global financial infrastructure.

SWIFT provides a secure and standardized messaging system for financial institutions to communicate and exchange information, but it does not hold funds or manages accounts

Ownership

SWIFT is owned by its member institutions, which are primarily banks and other financial institutions. It operates as a member-owned cooperative, with each member holding a stake in the organization based on their usage of SWIFT services. The governance of SWIFT is overseen by a Board of Directors, which is elected by its shareholders and comprises representatives from various member institutions.

How SWIFT operates

SWIFT provides a secure, standardized, and reliable messaging platform for financial institutions to exchange information. It uses a system of unique codes, known as Bank Identifier Codes (BICs) or SWIFT codes, to identify the sending and receiving institutions involved in a transaction. The messages sent via SWIFT are formatted according to specific message types and follow the ISO 20022 messaging standard, which ensures that the information exchanged is consistent, accurate, and easily interpretable by all parties involved.

Nature of SWIFT messages

It is important to note that SWIFT itself does not transfer money or hold accounts on behalf of its member institutions. Instead, SWIFT serves as a messaging system that facilitates the exchange of financial information, such as payment instructions, between banks and financial institutions. When a bank sends a payment instruction via SWIFT, it is essentially requesting the receiving bank to transfer a specified amount from its account to the beneficiary's account. The actual transfer of funds takes place through correspondent banking relationships and settlement systems, such as RTGS systems or Automated Clearing Houses (ACHs), which handle the movement of money between accounts.

Connection to SWIFT

Financial institutions connect to the SWIFT network through various channels, such as SWIFT Alliance Access, SWIFT Alliance Lite2, or SWIFTNet Link, depending on their size, technical capabilities, and messaging requirements. The messages are transmitted securely using SWIFT's proprietary communication protocol and encrypted using state-of-the-art security measures.

In summary, normal SWIFT transfers and communication rely on standardized MT messages and are gradually transitioning to the richer MX messages (ISO 20022) to facilitate cross-border transactions.

SWIFT Transfers and Communication with MT and MX messages

SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a secure messaging network that enables financial institutions, such as banks, to send and receive standardized messages about financial transactions, like payment instructions and confirmations. SWIFT does not hold accounts or transfer funds; it simply provides a secure and reliable platform for exchanging information.

Normal SWIFT transfers use a series of standardized message types known as MT (Message Type) messages. These messages have predefined formats and fields, ensuring that financial institutions can easily understand and process the information they contain.

MX (ISO 20022) messages are a newer standard of financial messaging based on XML (eXtensible Markup Language). They provide a richer and more structured format, allowing for enhanced data exchange and improved straight-through processing. MX messages are gradually replacing MT messages in the SWIFT network, with the aim of providing better interoperability and data handling capabilities.

While traditional SWIFT transfers have been the backbone of international payments for decades, they have some limitations, including limited transparency, slower processing times, and unstructured data, as I explained in the previous response.

Swift Currency Transfer Structure

Through Correspondent Banks. Correspondent banking relies on bilateral trust and the adjustment of balances on private ledgers (Nostro and Vostro accounts). This system carries higher credit risk because a Nostro account is essentially an unsecured loan to the correspondent bank. If a correspondent bank fails before the funds are passed along the chain, the requesting/receiving bank may suffer a loss.

Chain Dependencies: Correspondent banking often involves a chain of intermediaries, requiring multiple sequential updates to separate ledgers. Any failure or delay at one "hop" in the chain can stall the entire transaction.

Settlement typically happens via correspondent banking relationships (nostro/vostro accounts), bilateral netting, or Clearing and Settlement Mechanisms (CSMs) such as Real-Time Gross Settlement (RTGS) systems (e.g., TARGET2 in Europe, Fedwire in the US, or CHAPS in the UK).

Two Level Structure (Instruction/Information - & actual Funds Transfer-Level)

Two Level Structure (Instruction/Information - & actual Funds Transfer-Level)

With the SWIFT ISO 20022 migration nearing completion (coexistence phase ends November 2025), processes increasingly use SWIFT MX (ISO 20022) messages, though MT formats may still apply in some cases.

SWIFT MT Standards 2023

Category 1 - Customer Payments and Cheques

Message Reference Guide MT 101-199

Category 2 - Financial Institution Transfers

Message Reference Guide MT 200-299

Category 3 - Treasury Markets - Foreign Exchange, Money Markets and Derivatives

Message Reference Guide MT 300-349

Message Reference Guide MT 350-399

Message Usage Guide

Category 4 - Collections and Cash Letters

Message Reference Guide MT 400-499

Category 5 - Securities Markets

Message Reference Guide MT 500-518

Message Reference Guide MT 519-543

Message Reference Guide MT 544-567

Message Reference Guide MT 568-599

Message Usage Guide

Category 6 - Reference Data - Treasury Markets - Commodities

Message Reference Guide MT 600-699

Message Reference Guide MT 670-699

Category 7 - Documentary Credits and Guarantees/Standby Letters of Credit

Message Reference Guide MT 700-799

Category 8 - Travellers Cheques

Message Reference Guide MT 800-899

Category 9 - Cash Management and Customer Status

Message Reference Guide MT 900-999

Category n - Common Group Messages

Message Reference Guide MT n90-n99

FIN

System Messages

Error Codes

SWIFT MX Standards

Bank Account Management

Bank Services Billing

Bank-to-Customer Cash Management

Cash Management

Collateral Management

Corporate Actions

- Message Definition Reports and Schemas (11.2023) Part 1, Part 2, Part 2 Variants

Cross-Border Payment Reporting plus (CBPR+)

Exceptions and Investigations

Funds

General Meeting

Notification to Receive

Payments Clearing and Settlement

Payments Initiation

Payments Mandates

Post Trade Matching

Securities Clearing

Settlement and Reconciliation

- Message Definition Reports and Schemas (11. 2022) Part 1, Part 2, Part 2 Variants

- Message Usage Guidelines (06 June 2014)

Shareholders Identification Disclosure

Technical

Total Portfolio Valuation Report

Trade Services Management

Triparty Collateral Management

SWIFT STP Procedure

SWIFT (Society for Worldwide Interbank Financial Telecommunication) provides a network that enables financial institutions worldwide to send and receive information about financial transactions in a secure, standardized, and reliable environment. SWIFT does not actually transfer funds, but instead sends payment orders, which must be settled by correspondent accounts that institutions have with each other.

To clarify the role of Straight Through Processing (STP) in the context of SWIFT MT 103 and MT 202 COV messages, let's focus on how STP enhances the efficiency and accuracy of these transactions.

Straight Through Processing (STP) in SWIFT Transactions

STP refers to the automated processing of payments without the need for manual intervention. This process is crucial in the financial industry for ensuring fast, accurate, and cost-effective transactions.

STP in the Context of MT 103 and MT 202 COV:

- Automated Processing of MT 103 or MT 103+:

- When a bank sends an MT 103 message for a customer transaction, the STP system automatically processes this message.

- The system checks for completeness and accuracy of information, ensuring adherence to the required formats.

- If the message meets all criteria, it's forwarded automatically to the beneficiary's bank via the SWIFT network.

- STP in MT 202 COV for Interbank Settlement:

- Alongside MT 103, an MT 202 COV message is often generated for interbank fund transfer.

- STP systems automatically link MT 103 and MT 202 COV messages, ensuring that the cover payment corresponds to the actual customer transaction.

- The system checks the MT 202 COV for regulatory compliance, especially regarding the transparency of the originator and beneficiary details (as required in COV messages).

- Reduced Errors and Delays:

- By automating the processing, STP minimizes the risk of human errors and delays.

- It ensures that the transactions comply with international standards and regulations.

- Efficient Handling of Exceptions:

- In cases where transactions do not meet STP criteria (due to format errors, missing information, etc.), they are flagged for manual review.

- This exception handling is a crucial part of STP, ensuring that non-compliant or suspicious transactions are scrutinized.

- Rapid Settlement:

- STP enables quicker settlement of transactions as the automated process reduces the time taken for verification and transmission.

- This is especially critical in international transactions where speed is a key factor.

Summary

- STP in MT 103: Automates the processing of customer payment instructions, ensuring fast and accurate transaction handling.

- STP in MT 202 COV: Facilitates automated linkage and processing of interbank settlements related to customer transactions, with a focus on compliance and efficiency.

- Overall Impact of STP: Enhances the efficiency, accuracy, and compliance of financial transactions, reducing manual intervention and associated risks.

Swift 103+ STP (Straight Through Processing)

Swift 103+ STP is a format optimized for Straight Through Processing (STP). STP enables the entire payment process, from initiation to final settlement, to be conducted electronically without the need for manual intervention.

Additional Features:

- Standardized Format: It requires strict adherence to a standardized format, reducing errors and delays.

- Automated Processing: Transactions are processed automatically, ensuring faster and more efficient processing.

- Reduced Manual Intervention: The need for manual entry and verification is minimized, reducing the risk of errors and delays.

- Faster Settlement: Transactions are settled more quickly compared to traditional methods.

Considerations for STP:

- Accurate Data Entry: Data must be accurately input to avoid delays or rejections.

- Compliance with Format Requirements: Banks must ensure that the format requirements of 103+ STP are strictly followed.

- Software and Systems: Banks need to have appropriate software and systems in place to handle STP effectively

It is essential to distinguish between messaging and settlement. SWIFT transmits structured financial messages between institutions, but it does not itself move funds or hold balances. A SWIFT confirmation, including an MT103 message, is only valid when it corresponds to an actual transaction processed and reconciled within the banking systems of the participating institutions.

Any standalone SWIFT document, screenshot, or message presented without institutional verification should not be treated as evidence of completed settlement.

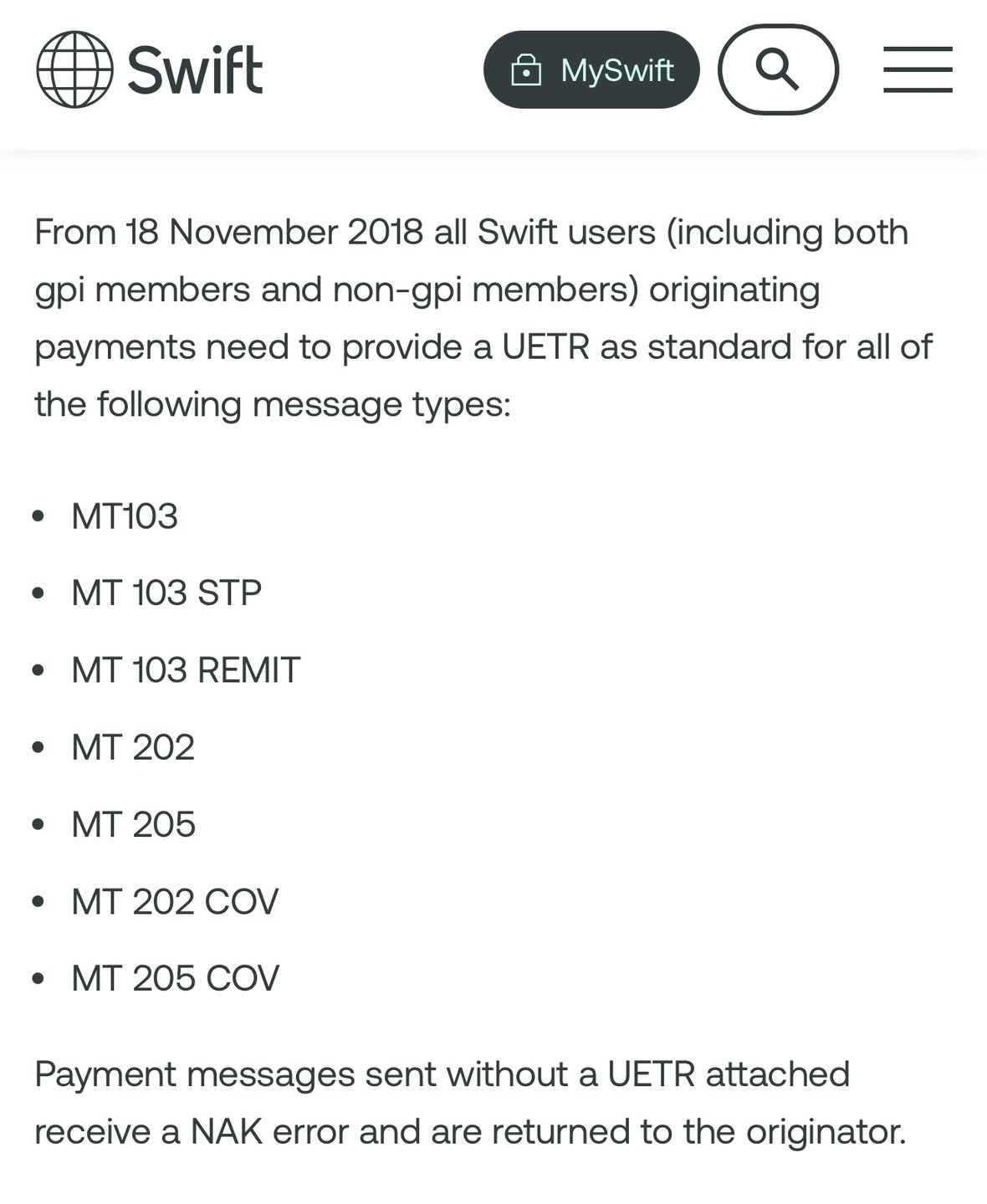

A SWIFT MT 103 STP

message requires a Unique End-to-End Transaction Reference (UETR). Since November 2018, all SWIFT users, including both gpi and non-gpi members, must include a UETR for various message types such as MT103, MT103 STP, and others.

SWIFT gpi transfers.

SWIFT gpi (Global Payments Innovation):

Launched in 2017, SWIFT gpi is an initiative designed to address the limitations of traditional SWIFT transfers by enhancing the speed, transparency, and traceability of cross-border payments. SWIFT gpi leverages the existing MT and MX message formats to improve payment services. Key features of SWIFT gpi include:

- Faster payments: gpi streamlines processes and establishes tighter service-level agreements (SLAs) between banks, resulting in faster transaction times, often within minutes or seconds.

- Payment tracking: The gpi Tracker enables real-time tracking of transactions, improving transparency and reducing manual investigations.

- Fee transparency: Banks can provide customers with information about transaction fees upfront, allowing for better decision-making.

- Richer data: gpi supports more detailed and structured information exchange, facilitating improved reconciliation and regulatory compliance.

SWIFT gpi addresses the limitations of traditional SWIFT transfers by enhancing cross-border payments with end-to-end tracking, faster processing, and richer data.

Unraveling the Semi-Automatic and Automatic Parts of the Swift gpi Processes

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) revolutionized international transactions with the introduction of its Global Payments Innovation (gpi). The primary goal of SWIFT gpi is to modernize and automate cross-border payments, ensuring speed, traceability, and transparency.

The Automatic Process: GPI Bank to GPI Bank

When both the sending and receiving banks are gpi members, the process can be fully automated. This makes the transaction faster, more efficient, and eliminates potential errors that may occur during manual processing. It enables real-time tracking of payments from start to end, providing a level of transparency previously unseen in cross-border transactions.

The Semi-Automatic Part of the Process:

Non-gpi Bank to gpi Bank or gpi Bank to non-gpi Bank

The semi-automatic gpi process comes into play when a transaction is initiated by a non-gpi bank to a gpi member bank. This transaction starts manually and becomes automated once it reaches the gpi member bank. If the non-gpi bank does not populate SWIFT fields 121 and 111, it becomes the responsibility of the first gpi member bank in the transaction chain to complete these fields accordingly thus ensuring the transaction meets the gpi standards for tracking and service level identification.

- Field 121 (Unique End-to-End Transaction Reference - UETR): This field is used to identify a payment transaction throughout its entire life cycle. It's a mandatory field for all gpi transactions, and each transaction must have a unique UETR.

- Field 111 (Service Type Identifier): This field is used to indicate the type of service, or level of urgency, required for a transaction. For example, a value of 001 indicates a normal payment, whereas 002 specifies a high priority payment.

At the initiation stage, a manual input of transaction details is required, including the beneficiary's information, amount, currency, and purpose of the transfer. This initial process is necessary as the non-gpi bank might not have systems in place to automate this part of the transaction.

The semi-automatic process then allows for a human to manually review the transactions to ensure compliance with regulations, such as Anti-Money Laundering (AML) and Know Your Customer (KYC) rules. Large or non-standard transactions may also require manual authorization or approval, ensuring they meet specific risk management or policy criteria.

Human Intervention can stop the Automatic Processes

Despite the predominant automation, certain circumstances could require human intervention, even in fully automatic gpi transactions.

- Fraud Detection: If a system flags potential fraudulent activity, a transaction might be halted for human review. This could be due to patterns that match known fraud methods, unusually large transfers, or transactions involving regions or parties with a high risk of fraud.

- Recall Requests: If a recall request is made for a transaction (e.g., due to an error or a detected fraud), a human may need to intervene to process the recall, particularly if the recall request is complex or requires coordination between multiple parties.

- Regulatory and Compliance Concerns: Automatic transactions might be paused for human review if they involve countries or entities subject to sanctions, or if there are other compliance concerns. This review can help ensure the transaction complies with all applicable regulations.

- Technical Issues: In the event of a system outage, bug, or other technical problems, human intervention might be required to fix the issue and ensure the transaction is processed correctly.

While SWIFT gpi's key promise lies in automation and efficiency, the reality of global financial transactions means there is still a role for human oversight. This blend of semi-automatic and automatic processes, paired with the necessary human intervention, allows the SWIFT gpi system to cater to a broad range of needs, while maintaining the highest standards of speed, security, and compliance.

Key Parameters for Non-SWIFT gpi Participants

When a non-SWIFT gpi participant (e.g., a bank or financial institution not directly enrolled in gpi) sends a payment instruction to a gpi participant bank, the gpi bank can convert it into the required SWIFT message formats (MT 103 for customer credit transfers, MT 202 COV for cover financial institution transfers, pacs.008 for ISO 20022 customer credit transfers, and pacs.009 for ISO 20022 financial institution credit transfers). This conversion enables processing and tracking within the gpi network, provided the instruction includes sufficient data to populate mandatory fields and comply with gpi rules, such as end-to-end traceability.

Non-gpi participants typically provide these parameters via domestic payment schemes, APIs, or legacy formats, and the gpi bank handles gpi-specific additions (e.g., generating a UETR if not supplied, though passing it is optional for non-gpi entities). The exact requirements may vary by jurisdiction, currency, and bilateral agreements, but the core parameters are drawn from CBPR+ (Cross-Border Payments and Reporting Plus) guidelines and ISO 20022 standards. Note that as of late 2025, with the ongoing ISO 20022 migration, conversions between MT and MX formats (like pacs.008/009) are supported during coexistence, but full MX adoption is approaching.

1. Party Identification (Debtor and Creditor Details)

These identify the originator and beneficiary, ensuring compliance with FATF Recommendation 16 for travel rule requirements.

- Debtor/Ordering Customer: Full name, structured address (street, city, postal code, country), and account identification (e.g., IBAN or account number). For MT 103/MT 202 COV, this maps to Field 50a; for pacs.008/pacs.009, to <Dbtr> and <DbtrAcct>.

- Creditor/Beneficiary Customer: Full name, structured address, and account identification. Maps to Field 59a in MT 103/MT 202 COV; <Cdtr> and <CdtrAcct> in pacs.008/pacs.009.

- Ultimate Debtor/Creditor (if applicable): If different from the primary parties, include their details for enhanced transparency (optional but recommended for gpi tracking). Maps to <UltmtDbtr>/<UltmtCdtr> in pacs.008/pacs.009.

Why required: Enables accurate routing and regulatory checks; incomplete data may lead to rejects or delays.

2. Agent and Routing Information

Specifies the financial institutions involved in the chain.

- Debtor Agent: BIC (Bank Identifier Code) or other identifier of the sending bank. Maps to Field 52a in MT 103; <DbtrAgt> in pacs.008/pacs.009.

- Creditor Agent: BIC of the receiving bank. Maps to Field 57a in MT 103/MT 202 COV; <CdtrAgt> in pacs.008/pacs.009.

- Intermediary Agents (if known): BICs for any correspondents (up to 3 levels). Maps to Field 56a in MT; <IntrmyAgt1-3> in pacs.008/pacs.009.

- Instructing/Instructed Agents: BICs for the immediate sender/receiver in the chain. Optional but aids in serial or cover methods.

- Previous Instructing Agents (if applicable): For multi-hop chains, up to 3 prior agents.

Why required: Ensures proper intermediary routing; use BICFI over names for precision in pacs.009 COV.

3. Transaction Details

Core financial elements for settlement.

- Amount and Currency: Interbank settlement amount and ISO 4217 currency code (e.g., USD, EUR). Maps to Field 32A in MT 103/MT 202 COV; <IntrBkSttlmAmt> in pacs.008/pacs.009.

- Instructed Amount (if different): Original amount before deductions.

- Interbank Settlement Date: Value date for settlement. Maps to part of Field 32A in MT; <IntrBkSttlmDt> in pacs.008/pacs.009.

- Settlement Method: Indicate if via RTGS (CLRG), cover (COVE), or agent (INDA/INGA). No direct MT equivalent but implied.

Why required: Defines the value transfer; mandatory for all formats.

4. Reference and Tracking Identifiers

For traceability, especially in gpi.

- End-to-End Identification: A reference linking the entire chain (e.g., invoice or transaction ID). Maps to Field 20C::E2EI in MT; <EndToEndId> in pacs.008/pacs.009.

- Instruction Identification: Sender’s reference (limited to 16 characters in MT). Maps to Field 20 in MT; <InstrId> in pacs.008/pacs.009.

- Unique End-to-End Transaction Reference (UETR): A UUID for gpi tracking. Non-gpi can provide it optionally; otherwise, the gpi bank generates it. Mandatory in pacs.008/pacs.009 for gpi; placed in Field 121 in MT 103/MT 202 COV.

- Transaction Identification: Additional internal reference.

Why required: Enables gpi tracking and linking (e.g., pacs.008 to pacs.009 COV); UETR is key for universal confirmations.

5. Purpose and Service Information

Classifies the payment type.

- Purpose Code (Category Purpose): ISO code (e.g., SALA for salary) to indicate transaction nature. Mandatory for many cross-border payments; maps to Field 23B/26T in MT or <CatPurp> in pacs.008/pacs.009.

- Service Level Code: For gpi priority (e.g., G001/G004), but non-gpi should not include gpi-specific codes like /gpi/ unless agreed. Maps to Field 23E in MT; <SvcLvl> in pacs.008/pacs.009.

- Local Instrument Code: For specific schemes (e.g., intragroup transfers).

Why required: Ensures regulatory compliance and processing priority; increasingly mandatory post-ISO migration.

6. Remittance and Additional Instructions

- Remittance Information: Unstructured (up to 140 characters) or structured (e.g., invoice details). Maps to Field 70 in MT 103; <RmtInf> in pacs.008/pacs.009.

- Instructions for Agents: E.g., /REC/ for receiver, /ACC/ for account, or phone instructions (PHOB). Maps to Field 72 in MT; <InstrForNxtAgt>/<InstrForCdtrAgt> in pacs.008/pacs.009.

- Settlement Time Indicators: Requested times (e.g., CLSTm for CLS time).

Why required: Provides context and handling instructions; essential for cover methods in MT 202 COV/pacs.009 COV.

7. Regulatory and Compliance Data

- Regulatory Reporting: Codes or details (e.g., tax ID, reporting indicator like CRED/DEB). Maps to Field 77B in MT; <RgltryRptg> in pacs.008/pacs.009.

- Return Reason Codes (if applicable for returns): E.g., AC04 for closed account, in pacs.004 linked to original messages.

Why required: Meets AML/KYC and reporting obligations; mandatory in regulated corridors.

For best practices, non-gpi participants should structure data to avoid truncation during MT-to-MX conversions and consult the gpi member bank for specific needs. If the payment involves cover methods, the underlying customer details must mirror across messages (e.g., MT 103 to MT 202 COV).

Payment Messages in SWIFT gpi

In the SWIFT gpi (Global Payments Innovation) framework, the original payment messages (e.g., MT 103 for customer transfers or MT 202 COV for cover transfers) are considered immutable once sent. Receiving banks cannot directly alter or modify the content of these messages, as SWIFT messages are designed to maintain integrity and auditability throughout the payment chain. Instead, any changes, corrections, or cancellations are handled through separate follow-up messages, status updates via the gpi Tracker, or dedicated services like gSRP (gpi Stop and Recall Payment). This ensures end-to-end traceability using the Unique End-to-End Transaction Reference (UETR).

Receiving banks (typically acting as the creditor agent or intermediary) can, however, respond to alteration requests from the sender or initiate actions that effectively result in modifications to the payment outcome (e.g., returns or holds). They can also request clarifications or amendments from the sender under specific conditions. These processes are governed by SWIFT’s rulebooks, market practice guidelines (e.g., from the Payments Market Practice Group - PMPG), and regulatory requirements, prioritizing automation, transparency, and fraud prevention.

Conditions for Receiving Banks to Request or Facilitate Alterations

Receiving banks may request alterations (e.g., corrections to details) or take actions that imply a need for change when the original payment cannot be processed as instructed. This is typically done via inquiry messages (e.g., MT 195/199) or responses to sender-initiated requests. Key conditions include:

- Errors in Payment Details: If there are inaccuracies such as incorrect beneficiary account (e.g., closed account - code AC04), wrong currency (code CURR), incorrect agent routing (code AGNT), or technical issues (code TECH), the receiving bank can place the payment on hold and request the sender to provide corrected information or send a new payment. This avoids outright rejection while allowing resolution.

- Inability to Apply the Payment: Under code CUTA (Cancel Upon Unable to Apply), if the payment cannot be credited due to mismatches (e.g., name/account discrepancy or insufficient details), the receiving bank can request cancellation or amendment details from the sender to remediate.

- Suspected Fraud or Unauthorized Transactions: For fraud (code FRAD), the receiving bank can independently detect issues and initiate a return of funds without a prior request from the sender. They can also respond to sender’s recall requests by quarantining funds and requesting indemnity (code INDM) if funds are already credited, to mitigate risk before returning.

- Duplicate or Undue Payments: Codes like DUPL (duplicate payment) or UPAY (undue payment) allow the receiving bank to flag and request cancellation if the transaction is erroneous or unjustified.

- Regulatory or Compliance Issues: If the payment violates local laws, sanctions, or AML requirements (code LEGL), the receiving bank can reject or hold it and request additional documentation or amendments from the sender.

- Customer or Beneficiary Decisions: If the beneficiary refuses the payment (code CUST or NOAS - no answer from beneficiary), the receiving bank can return it and notify the sender, potentially requesting confirmation of changes.

- Pending Resolutions: For pending cases (code PDCR), such as awaiting debit authority (RQDA) or reply from next agent (PTNA), the receiving bank can hold the payment and request further instructions or alterations to proceed.

In all cases, requests must be structured for automation (e.g., including UETR, original references like field 20/32A/50/59, and specific codes in field 79 of messages) to support straight-through processing. Indemnity agreements may be required bilaterally if funds are credited, and the receiving bank has no obligation to accept requests but must prioritize urgent ones (e.g., fraud-related).

Processes Involved

- Response to Sender-Initiated Recalls: The sender (debtor agent) typically initiates a recall via MT 192/292 (or ISO 20022 equivalents like camt.056) through the gSRP service, sent serially or directly to the receiving bank. The receiving bank must acknowledge immediately and respond with MT 196/296 (or MT 199/299 if structured), using codes like CNCL (cancelled), RJCR (rejected with reason), or PDCR (pending). If accepted, funds are returned via MT 202/103. Direct contact (e.g., MT 992 without RMA) can expedite for fraud.

- Independent Actions by Receiving Banks: If fraud is detected internally, the receiving bank can return funds using MT 202/103 with structured details, notifying via the Tracker for real-time status updates.

- Requests for Amendment/Clarification: Receiving banks use inquiry messages (e.g., MT 195/295) to request changes, such as additional details (code 23/33 for amendments). This is common for on-hold payments (e.g., code 48-52 for blocked status).

- Tracker Integration: All actions update the gpi Tracker in real-time, accessible via APIs or GUI, ensuring visibility for all parties. gpi members must comply with mandatory rulebooks for gCCT (Customer Credit Transfer), gCOV (Cover), and gSRP.

- Limitations and Success Factors: Alterations are not guaranteed; success depends on the payment stage (easier pre-crediting), beneficiary cooperation, and jurisdiction. If credited, returns require beneficiary consent or indemnity. Regulations always supersede guidelines.

These practices apply primarily to gpi members, but non-gpi banks can participate via gateways. For the most current details, consult SWIFT’s official rulebooks, as processes evolve (e.g., with ISO 20022 migration).

Separation of Messaging and Settlement in SWIFT gpi

SWIFT gpi primarily handles payment instructions and tracking through messaging (e.g., ISO 20022 formats like pacs.008 for customer transfers, pacs.009 for financial transfers, or legacy MT 103/MT 202), but the actual movement of money occurs separately at the settlement level. Settlement typically happens via correspondent banking relationships (nostro/vostro accounts), bilateral netting, or Clearing and Settlement Mechanisms (CSMs) such as Real-Time Gross Settlement (RTGS) systems (e.g., TARGET2 in Europe, Fedwire in the US, or CHAPS in the UK). The gpi Tracker provides real-time visibility into message status, but funds transfer relies on these underlying systems.

With the SWIFT ISO 20022 migration nearing completion (coexistence phase ends November 2025), processes increasingly use MX (ISO 20022) messages, though MT formats may still apply in some cases. Below, I explain how returns and hold releases occur at the account/clearing/settlement level.

How Money is Returned at the Account/Clearing/Settlement Level

Returns are initiated after a successful recall request (via gSRP - gpi Stop and Recall Payment service) or independent detection (e.g., fraud, errors). The gSRP uses messages like camt.056 (Payment Cancellation Request) from the sender, with responses via pacs.010 (Payment Return) or pacs.002 (status update). Once accepted, the return of funds is executed through a new payment instruction that reverses the flow, debiting the receiving bank’s account and crediting back through the chain. This is not an alteration of the original message but a separate transaction.

Key Settlement Methods and Return Processes

Settlement methods dictate how returns occur:

- CLRG (Clearing via Market Infrastructure): Settlement through an RTGS or CSM (e.g., via a central bank). Returns use pacs.004 to instruct the MI to debit the receiving agent’s account and credit the prior agent’s, often in real-time or same-day.

- INGA (Instructing Agent Settles First): Sender settles funds before messaging. Returns via pacs.004 debit the instructed agent’s account post-settlement.

- INDA (Instructed Agent Settles on Receipt): Receiver settles upon message receipt. If unsettled, reject via pacs.002 (no funds move); if settled, return via pacs.004.

- COVE (Cover Method): Used for high-value payments with a cover transfer (pacs.009 COV). Returns follow the reverse chain: pacs.004 from the beneficiary agent back to intermediaries, debiting/crediting correspondent accounts accordingly.

Step-by-Step Return Process at Settlement Level

1. Initiation and Acceptance: Sender requests recall (e.g., via camt.056 with UETR). Receiver acknowledges (pacs.002) and accepts if funds are available/not yet credited to beneficiary (easier pre-crediting). If credited, beneficiary consent or indemnity may be required.

2. Funds Return Instruction: Receiver issues pacs.004 (Payment Return) or legacy MT 103/MT 202 with return codes (e.g., RETN). This message includes:

- Original references (UETR, End-to-End ID, Instruction ID).

- Reversed roles: Original creditor becomes debtor; original debtor agent becomes creditor.

- Settlement details: Original Interbank Settlement Amount/Date, Exchange Rate (if FX involved), Charges (if deducted).

- Return Reason Code (e.g., AC04 for closed account, FRAD for fraud).

- Settlement Account field (if in original message) to specify the account for credit.

3. Settlement Execution:

- The pacs.004 triggers debit from the receiving bank’s nostro/vostro account (held with the prior agent or MI).

- Funds are credited back hop-by-hop through the chain, using the same settlement method (e.g., RTGS transfer in CLRG).

- If partial return, specify “PART” in Additional Information with prorated amount.

- Tracker updates status (e.g., “Returned”) in real-time, visible via API or GUI.

4. Final Credit: Original sender’s account is credited, often with deductions for fees. If via CSM, settlement is atomic; in bilateral setups, it may involve end-of-day netting.

5. Post-Return Notifications: Use camt.053/054 (Account Statement/Debit-Credit Notification) to confirm ledger updates. No further pacs.004 for “returning a return”—use inquiries instead.

Returns are automated where possible, but manual intervention may occur for compliance or if funds are frozen. Success rates are higher for fraud (up to 25% funds recovered via gSRP), and gpi mandates same-day processing where feasible. If unsettled (e.g., rejected pre-settlement), no funds move—use pacs.002 instead.

How Held Payments Are Released (Green-Lighted) at the Account/Clearing/Settlement Level

Holds occur when a payment cannot be immediately processed (e.g., due to errors, compliance checks, or awaiting clarification), placing it in a “pending” state without settlement. No funds are debited/credited until resolution. The gpi Tracker shows statuses like “On Hold” or “Pending” (e.g., PDCR code), and resolution uses inquiry messages (MT 195/199 or camt.029).

Conditions Leading to Holds

- Mismatches (e.g., account/name discrepancy - CUTA code).

- Regulatory checks (e.g., sanctions - LEGL code).

- Awaiting beneficiary response (NOAS code) or debit authority (RQDA).

- Offline hours or batch processing at beneficiary bank.

Release Process at Settlement Level

1. Hold Notification: Receiver sends pacs.002 (status update) or MT 199 with pending code, holding funds in a suspense/escrow account if partially settled (e.g., in cover methods).

2. Resolution: Sender provides amendments/clarifications (e.g., via MT 195 response or camt.029). If resolved, receiver “green-lights” by processing the original instruction.

3. Settlement Execution:

- Original pacs.008/009 (or MT 103/202) is released from hold.

- Funds settle via the specified method: Debit sender’s account, credit receiver’s (e.g., via RTGS in CLRG), then final credit to beneficiary’s account.

- Beneficiary leg (receiver to end customer) is key—33% release in under 5 minutes, but delays common in regions with capital controls or low infrastructure.

- Tracker updates to “Credited” or “Completed,” with camt.057 (Payment Status Report) confirming.

4. If Not Released: If unresolved (e.g., after timeout), return via pacs.004 as above, or reject with pacs.002 (no settlement).

Releases aim for same-day crediting per gpi SLAs, with 60% of gpi payments overall credited within 30 minutes once processed. Factors like capital controls or bank offline hours can extend holds, but gpi emphasizes automation to minimize them.

For a general overview about SWIFT GPI please click here and for the Swift GPI Certified Application Manual please click here and for the Swift gpi Guidelines click here.

To check your UETR Unique End-to-End Transaction Reference (UETR) identifier that is now required on all cross border transactions processed via the SWIFT network through Deutsche Bank (please click here), through Standard Charter (please click here), through BNY Mellon (please click here), Wells Fargo (please click here), Santander (please click here) or TrackMySwift (please click here).

To understand other identifiers (please click here or here)

SwiftNet Instant

SwiftNet Instant. It is a real-time, low latency messaging platform that is available 24/7 and supports the secure exchange of instant payment flows between Clearing and Settlement Mechanisms (CSMs) and their participants.

Customers can connect to SwiftNet Instant through their existing Swift connectivity and security infrastructure, including VPN boxes, leased lines and hardware security modules. Integration with the bank’s IT environment is achieved through the Alliance Gateway Instant (AGI).

All parties along the instant payment chain can use AGI and SwiftNet Instant messaging. Applications include payment initiation from an overlay service, indirect member communications with a sponsoring member, or a corporate receiving a payment confirmation.

SWIFT Instant connects with domestic instant payment systems to enable real-time transaction processing, both domestically and internationally, using the ISO 20022 standard. These systems represent ongoing efforts to modernize and streamline payment processes in the financial industry.

SWIFT Direct Debit

SWIFT Direct Debit

Direct debit in the SWIFT system is a payment method that allows businesses and individuals to collect funds from debtor bank accounts in multiple currencies and across different countries. Unlike SEPA Direct Debit, which is specifically designed for the SEPA zone and is limited to euro-denominated transactions, direct debit in SWIFT has a global scope and supports a wide range of currencies.

The process of initiating a direct debit transaction within the SWIFT system typically involves the following steps:

- Agreement between creditor and debtor: The creditor and debtor must have a pre-existing agreement, which includes the terms and conditions for direct debit transactions. This agreement may also involve setting up a mandate or authorization, allowing the creditor to collect payments from the debtor's bank account.

- Message exchange: The creditor initiates the direct debit transaction by sending a SWIFT message (MT101 or MT204) to the debtor's bank. This message contains the details of the transaction, such as the amount, currency, debtor's account information, and any other necessary information.

- Verification and authorization: The debtor's bank verifies the transaction details, checks the availability of funds in the debtor's account, and confirms the authorization for the transaction. If everything is in order, the debtor's bank proceeds to debit the funds from the debtor's account.

- Funds transfer: The debtor's bank orders the transfer of the funds through its correspondent bank to the creditor's bank, usually via an MT202 message and informs the bank of the beneficiary with a MT103 message in the SWIFT system.

- Confirmation: Upon receiving the funds, the creditor's bank sends a confirmation message to the creditor, notifying them of the successful direct debit transaction.

The prerequisites for initiating a direct debit transaction within the SWIFT system are as follows:

- Bank accounts: Both the creditor and debtor must hold bank accounts with financial institutions that are part of the SWIFT network.

- Agreement and authorization: A pre-existing agreement and authorization (mandate) between the creditor and debtor must be in place to enable direct debit transactions.

- SWIFT message formats: The creditor must be familiar with the appropriate SWIFT message formats (e.g., MT204, MT202, MT103, MT101) used for initiating and completing direct debit transactions.

- Bank fees: The creditor and debtor should be aware of any fees associated with direct debit transactions within the SWIFT system, as these fees may vary depending on the banks and countries involved.

MT 101 Scope

This message is:

- sent by a financial institution on behalf of a non-financial institution account owner, to an account servicing financial institution or to a forwarding financial institution for further transmission to the account servicing institution.

- sent by a non-financial institution account owner, or a party authorised by the account owner, to an account servicing financial institution or to a forwarding financial institution for further transmission to the account servicing institution.

It is used to move funds from the ordering customer's account(s) serviced at the receiving financial institution or at the account servicing institution, or from an account(s) owned by the ordering customer which the instructing customer has explicit authority to debit, for example, a subsidiary account.

The MT 101 can be used to order the movement of funds:

- between ordering customer accounts, or

- in favour of a third party, either domestically or internationally.

MT 101 Format Specifications

The MT 101 consists of two sequences:

- Sequence A General Information is a single occurrence mandatory sequence and contains information to be applied to all individual transactions detailed in sequence B.

- Sequence B Transaction Details is a repetitive sequence; each occurrence provides details of one individual transaction. Fields which appear in both sequences are mutually exclusive.

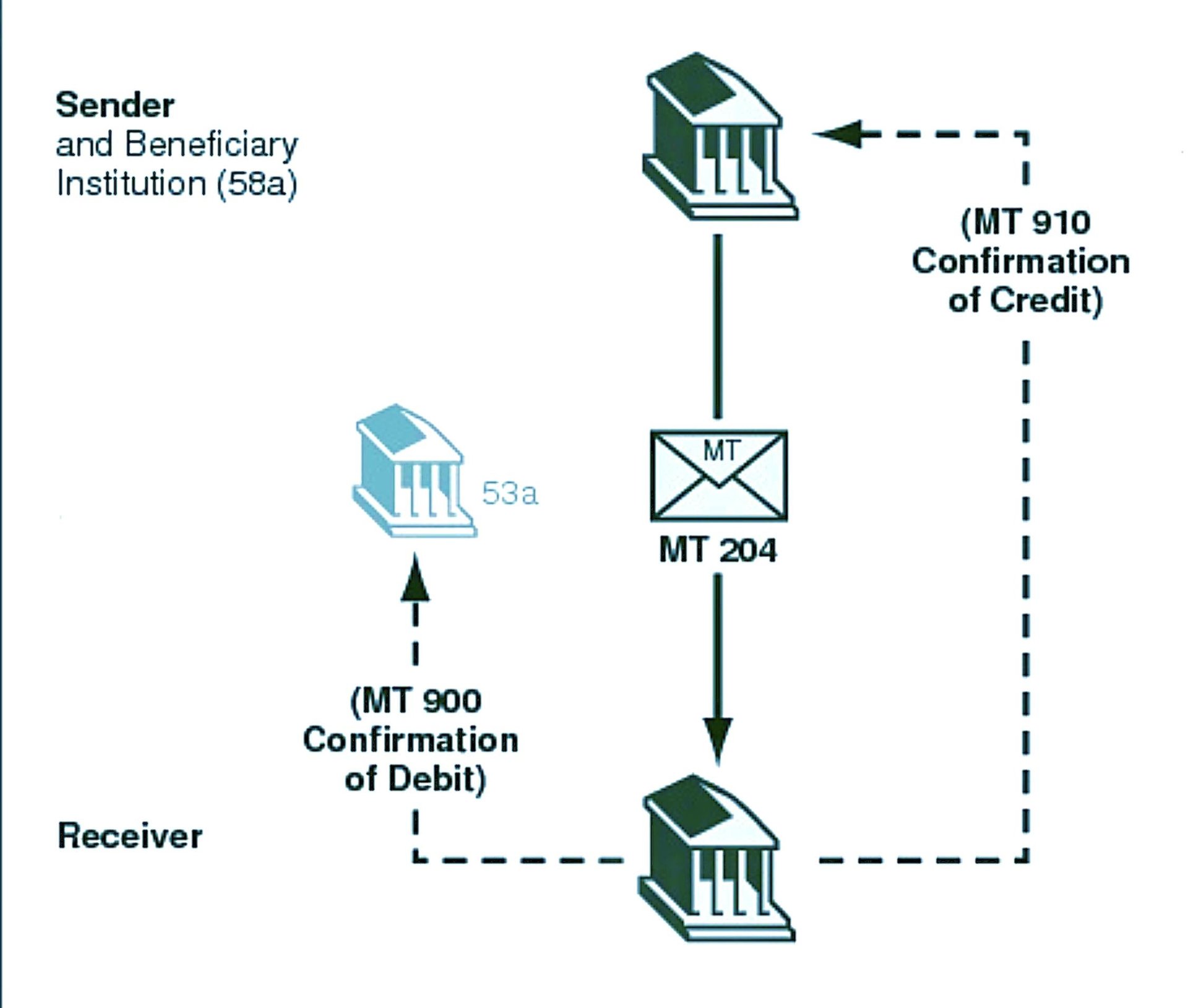

SWIFT MT204 message:

- Purpose: The MT204 message is specifically designed for General Financial Institution Transfer Instructions. It is used to instruct a financial institution to transfer funds between accounts, especially when dealing with treasury or money market operations.

- Structure: Like all SWIFT messages, the MT204 follows a structured format that includes a series of fields. Each field has a specific purpose, such as specifying the amount, currency, sender, receiver, and other transaction details. This structured format ensures consistency and clarity in financial communications.

- Participants: Typically, this message is exchanged between financial institutions, such as banks, rather than individual customers. It's an integral part of interbank communication for the execution of financial transactions.

- Security and Reliability: SWIFT messages, including the MT204, are known for their high levels of security and reliability. The SWIFT network provides a secure and standardized platform for financial institutions to communicate, which is crucial for maintaining the integrity and confidentiality of financial transactions.

- Use in Treasury and Money Markets: In the context of treasury and money market operations, the MT204 is used for transactions like fund transfers, settlement of trades, and other related financial activities. It facilitates the efficient and accurate processing of these transactions.

- Compliance and Standardization: The MT204, like other SWIFT messages, adheres to strict international standards, ensuring that it is compliant with global financial regulations and practices. This standardization is key to the smooth functioning of international financial markets.

RMA in Interbank SWIFT Messaging

In the realm of banking and finance, secure and efficient communication between banks is paramount. This is where SWIFT (Society for Worldwide Interbank Financial Telecommunication) plays a crucial role, facilitating nearly all international bank-to-bank messages. A critical component ensuring the security and selectivity of these communications is the Relationship Management Application (RMA). This article provides an in-depth exploration of how RMAs are performed between banks looking to exchange SWIFT messages, relevant for institutions like IFB Bank that engage in global financial transactions.

What is RMA?

Relationship Management Application (RMA) is a SWIFT software application that allows financial institutions to define which counterparties can send them SWIFT messages and ensures that SWIFT network communication is restricted to authenticated users only. RMA is a fundamental security layer in the management of interbank communication, as it filters out unauthorized messages and reduces the risk of fraud.

The Importance of RMA

For banks engaged in international finance, such as IFB Bank, the RMA tool is indispensable. It not only reinforces security protocols but also ensures compliance with global banking regulations. By managing which institutions can send messages to them, banks can prevent unauthorized information requests and financial instructions, protecting both their interests and those of their clients.

How RMA Works

The RMA process involves several key steps:

- Establishing RMA Relationships: Before two banks can begin exchanging information via SWIFT, they must mutually agree to establish an RMA. This agreement is akin to a digital handshake, signifying trust and consent to communicate.

- Exchanging Keys: As part of setting up an RMA, banks exchange SWIFTNet PKI (Public Key Infrastructure) certificates. These certificates are used to authenticate messages and ensure that they are only accessible to intended recipients.

- Configuring RMA Settings: Each bank uses the RMA tool to configure permissions and specify which types of messages are accepted from the other bank. This can be broadly categorized or finely tuned to include specific message types and subclasses.

- Activation and Monitoring: Once RMA settings are configured and activated, banks can monitor incoming messages for compliance with the established permissions. RMA also provides tools to modify or revoke permissions if business needs or security concerns dictate.

Practical Applications

For IFB Bank, which specializes in investment and wealth management for high-net-worth individuals and corporate entities, RMA provides several benefits:

- Enhanced Security: By controlling message traffic, IFB Bank can secure client transactions and sensitive information against unauthorized access.

- Operational Efficiency: Streamlined communications with trusted entities ensure faster processing of legitimate messages, improving response times and client satisfaction.

- Regulatory Compliance: RMA aids in compliance with international banking regulations, which mandate strict control over information exchange to prevent financial crimes such as money laundering and fraud.

Conclusion

For IFB Bank, effective implementation of RMA is not just a technical requirement but a strategic asset in its global operations. It reinforces the bank’s commitment to security and regulatory compliance, while enhancing the efficiency of its communication networks. As the landscape of international finance continues to evolve, tools like RMA remain essential in the arsenal of banks committed to maintaining the highest standards of operational integrity and client service.

In conclusion, RMAs form the backbone of secure and selective interbank communication, ensuring that every message exchanged via the SWIFT network adheres to the highest standards of security and is fully authenticated. For banks like IFB Bank, understanding and managing RMAs is crucial to safeguarding their operations and building trust with their global partners.

RMA Exchange Procedure

Swift Digital Blockchain Financial Instructions

Swift, in partnership with more than thirty leading financial institutions, has initiated the design and development of a shared digital ledger. The first application will focus on enabling real-time, 24/7 cross-border instructions between banks – a critical enhancement to the fabric of international transaction processing.

The blockchain-based ledger is being developed with Consensys as a secure, immutable, and real-time register of financial instructions between institutions. It will record, sequence, and validate transaction messages, while enforcing operational and compliance rules through smart contracts. Interoperability is a central principle: the ledger will connect with both existing and emerging infrastructures, while maintaining Swift’s hallmark resilience, trust, and regulatory adherence.

As Swift’s Chief Executive, Javier Pérez-Tasso, explained:

“Combining a shared ledger with Swift’s existing messaging, APIs and ISO 20022 creates an even more powerful construct – one that can embed risk, controls and compliance requirements from the outset into transaction flows while enabling real-time 24/7 interbank cross-border instructions with the same trust, security, resilience, scalability and operational excellence Swift is known for. All in line with the approach we’ve always taken of responsible innovation.”

Extension of Infrastructure

The shared ledger complements Swift’s existing rails; it does not replace them. It is designed to extend orchestration and interoperability, ensuring that financial institutions can exchange instructions faster, with greater predictability, and at a truly global scale.

At Sibos, Pérez-Tasso underlined this dual-track approach:

“Financial infrastructures need to keep relentless focus on the fundamentals of operational excellence, regulatory compliance and governance. And at the same time, they need to get ready for the future. And at Swift, our approach is to innovate across two parallel tracks.”

Collaboration Across the Industry

Over thirty leading banks from sixteen countries are actively engaged in shaping the design, governance, and development path of the shared ledger. This collective effort underscores a shared recognition: advancing the global infrastructure for interbank instructions requires scale and collaboration.

Looking Ahead

The shared ledger is a natural progression of Swift’s earlier digital asset trials and is part of a broader commitment to interoperability across both public and private networks. This will allow regulated tokenised value and traditional instruments alike to move seamlessly between systems.

Pérez-Tasso summarised the vision:

“This is a powerful platform for the future. And it can be even more transformational in the future.”

FAQs

What is the Swift blockchain-based shared ledger?

A blockchain infrastructure providing a shared, real-time record of financial instructions between institutions, enabling continuous, compliant, cross-border processing.

Who is it for?

Banks and financial institutions that must deliver faster, more transparent transaction instructions while preparing for the digital future.

What are the benefits?

- Real-time visibility and sequencing of instructions

- Automated compliance via smart contracts

- Interoperability across traditional and digital networks

- Secure handling of regulated tokenised value flows

How does it fit with Swift’s platform?

It extends Swift’s trusted infrastructure, embedding digital instruction capabilities while maintaining resilience, security, and compliance.

What is the first use case?

Real-time, 24/7 cross-border interbank transaction instructions.

Who is involved?

Over thirty major banks from sixteen countries, collaborating with Swift and Consensys.

When will it be available?

The initiative is being developed in stages, beginning with a conceptual prototype, followed by phased testing and refinement.

Do you still have questions?

Please book a Videoconference here:

Content from Calendly can't be displayed due to your current cookie settings. To show this content, please click "Consent & Show" to confirm that necessary data will be transferred to Calendly to enable this service. Further information can be found in our Privacy Policy. Changed your mind? You can revoke your consent at any time via your cookie settings.

If you want to know more about how to transfer funds through the corresponding banking system, please get in contact with our Head of Corresponding Banking M. Amri Elarisse